Spray, Pray, and Yap Away

It's All a Numbers Game

Welcome to Words with Wynn! If this is your first time perusing my content and you’d like more of my weekly musings, subscribe below:

I’m beginning to suspect that the art of accelerators is really just aura farming. Everything is sales, and venture is no different. You peel back the onion in incubator land and begin to see through the matrix. Sure, there’s a bit of intellectual butt-sniffing (founders pitching their vision, investors showcasing their ✨value add ✨), but the metagame in a world awash with VC dollars ultimately comes down to selling a perfectly substitutable product: cold hard cash.

This is why branding is key: perception is paramount. The venture profession is a funny kind of magic trick- finding the most brilliant people you can, and convincing them that your dollars have more value than those of your competitors.

That’s the matrix of all these incubators. There is no spoon, just a collection of strategies for getting on more cap tables earlier and culling thereafter.

The name of the game for many accelerators is to cast the broadest net possible, last long enough for statistics to do their thing, and then scream to high heavens about your early wins. Spray, pray, and yap away.

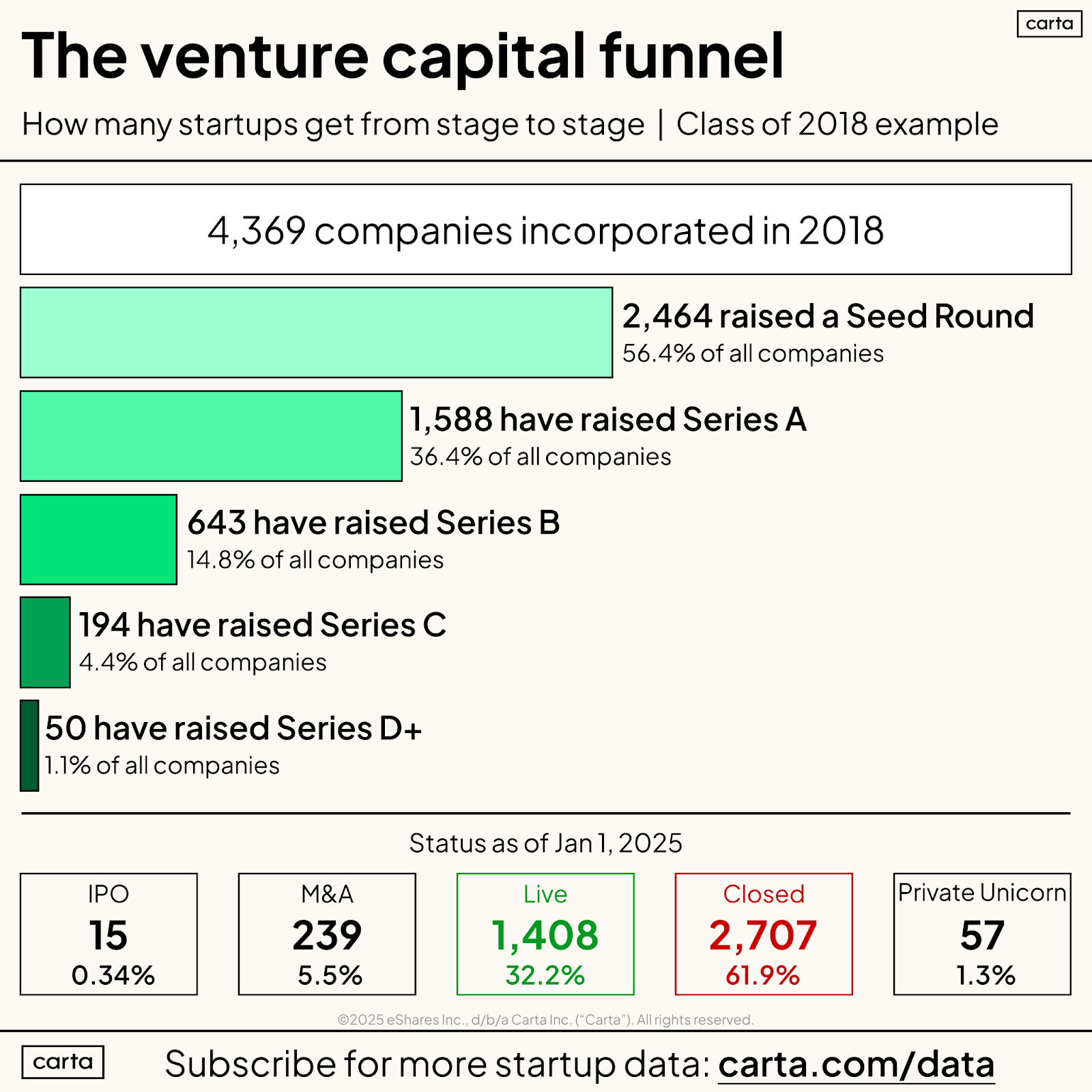

Investing in startups is a treacherous business, with only 1 out of every 3 making it to Series A, let alone IPO:

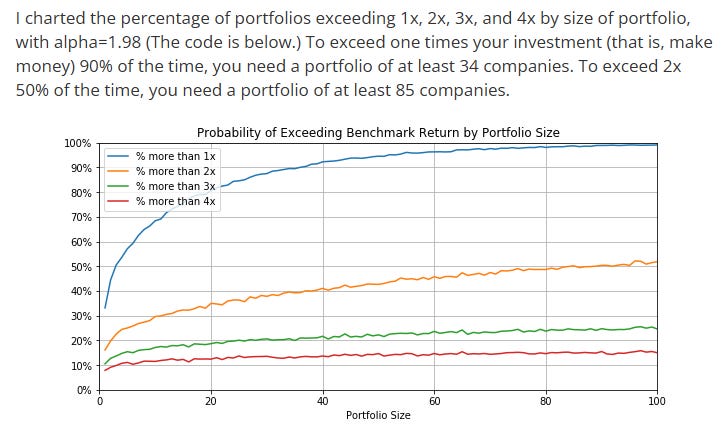

So, the earlier you go, the riskier it becomes, and the broader a net you should cast. This math is precisely why every accelerator works through much higher volumes (dozens of companies a year) than later stage investors that may pick about 15-20 companies per fund. In order for the Power Law to work its magic, there’s a sweet spot of how many bets you should place to optimize your odds of outperforming. If you want a gory analysis of the math, check out Jerry Neumann’s excellent post: Power Laws in Venture Portfolio Construction.

But in order to help skew the odds in your favor, regardless of portfolio size, there are three major components of the funnel to build:

Source better companies (improve the average quality of your dealflow)

Give your founders unfair advantages (support your bets better than the competition)

Double down on your winners (have a robust means of following on later)

The best firms do some mix of all three exceptionally well, but here we’ll discuss how different players construct the top of that funnel. This is the dealflow engine that VC’s use to fuel their later stage funds, typically securing some kind of proprietary access in subsequent rounds. There are many ways to skin this cat, and I’ll only be highlighting a few specific examples. But if you’re a founder looking to really get a lay of the land, I’ve consolidated a mega sheet here listing over a dozen of the most prominent accelerators/incubators and how their workflows look.

As I’m sure you’ve noticed, I’m using accelerator and incubator interchangeably for the sake of this piece. A pedantic investor might bifurcate these models into incubators for the earliest of early (pre-MVP, pre-revenue) and accelerators as a means of speeding growth (funding PMF, teaching GTM, supporting scaling). The way I’m thinking about them all here is as top of funnel for your later stage/follow-on funds to cherry pick the winners.

There are a few interesting permutations of early stage strategies in the pre-seed/seed arena, and I broadly classify them as Classic, Advisory (Sweat Equity), and Freemium.

Classic: Classic accelerators running a standard cohort-based support model.

Y Combinator - The creme de la creme of startup accelerators. YC is the darling of Silicon Valley, and known the world over for the caliber of its founders, funders, programming, and team, to say nothing of its elder statesman Paul Graham. YC runs four cohorts each year of around 125 companies (a recent shift from only two batches per year). Strategically, they’ve consolidated their might in Silicon Valley, after running bi-coastal programming between Boston and California in the early days. They invest in companies through the YC Standard deal:

3-month program, now run 4x a year

$125K SAFE for 7% ($1.8M post) + $375K uncapped MFN SAFE

Techstars - Techstars runs a cohort-based model similar to YC with a slightly different strategy for scaling. Techstars took a more national approach, partnering with cities and corporates to spin up localized programs, each run by a sector-specific managing director. In many ways, Techstars was both beneficiary of and contributor to the U.S. ‘technification’ wave as Silicon Valley began to dominate the U.S. economy and cities across the country pined to energize their own startup ecosystems. This was a net positive, but strategically created more of a federation of Techstars franchises than a monolithic brand like YC. They run over 50 accelerator programs across 30 locations, backing 700-800 companies a year. Ultimately, this decentralization has allowed Techstars to lean into city-specific superpowers (ex: fintech in NYC) while producing volume, building national brand aura, and securing pro rata across the board. The challenge though has been quality control, with founder experience relying more heavily on the caliber of the in-market manager. Techstars updated their investment terms a couple years ago, moving toward YC’s standard:

3-month accelerator program, with cohort cadence differing by market

$20K for 5% Convertible Equity Agreement + $200K uncapped MFN SAFE

Boost – Boost is not an accelerator, but a high-volume pre-seed fund with a number of accelerator-adjacent mechanisms for capturing particularly early deal flow. Adam Draper and Co. have built a stellar reputation as first check investors, moving with conviction and speed. The fund’s website says that they average one deal per week, investing $500K checks. On top of their traditional dealflow though, the Boost team capitalizes on specific thesis or extra early opportunities with a few other programs. They’ve created a Founders Start equity grant as well as topic-specific cohorts like their recent Bio Residency or pitch competitions with partner funds (s/o Arian and Earthling VC):

Residencies: $500K for 10% ($5M post); ~4 weeks

Pitch Competition: $100K SAFE for 4% ($2.5M post)

Founders Start Fellowship: $50K for ~3% ($1.5M post)

Fund checks $500K (val presumably TBD)

Advisory (Sweat Equity): Services and support in exchange for a nibble at the apple.

Capital Factory - Capital Factory is the biggest, baddest ecosystem builder in the state of Texas. The Austin based firm runs a sprawling collection of businesses including major conferences, coworking, founder education, corporate scouting, ecosystem building, a DARPA Commercial Accelerator, and a family of funds. The team has evolved a unique model for supporting founders at scale through its All Access program, which engages around 100 companies a year. All Access is more akin to bringing an institutional advisor onto the cap table than a formalized 13-week accelerator program. What this means in practice is that startups exchange $100K worth of equity (capped at 1% ownership) for access to a suite of services to support their scaling. This includes everything from Capital Factory’s dedicated investor relations team through its corporate partnerships and Defense Innovation Center. It’s a lifelong relationship where founders can tap the various components of Capital Factory’s platform as their challenges evolve. This structure and ecosystem approach also allow Capital Factory to engage companies across the lifecycle of their business. The capped $100K equity grant is less dilutive for later stage companies and drives a broader collection of founders within the ecosystem orbit. This, in turn, helps to engage a deeper set of partners- corporates, defense partners, multi-stage investors. Intrinsic to the agreement is a guaranteed allocation in the startup’s next priced round, which helps to feed Capital Factory’s follow-on vehicles.

Lifelong relationship; year-round, ongoing support centered around cornerstone events

$100K advisory equity granted, capped at 1% ownership

Fund checks ranging from $100-$250K

Freemium: Offering resources for founders, as a means of getting them in the door.

Plug and Play - Plug and Play is a bit like an external innovation arm for corporate partners, acting as a sounding board for their biggest problems and then sourcing startups to solve them at scale. What originally started in the Lucky Building in San Francisco (early office space of Google and PayPal), has now expanded globally to 125 accelerators working with over 2,500 startups each year. What differentiates Plug and Play is its equity-free accelerator offering. The firm has aggregated over 500 global corporates for whom it scouts startups; these partnerships subsidize the cost of Plug and Play’s programming. This arrangement is mutually beneficial as it offers founders close access to corporate partners, which may result in customer relationships, while simultaneously giving Plug and Play a privileged look into the market’s appetite for various startup solutions. The team is then able to accelerate traction achieved through their matchmaking with investment from their fund thereafter (investing in over 200 startups a year). Additionally, as opposed to others listed here which focus pre-seed/seed, both Plug and Play’s accelerator and its fund are stage agnostic, which aligns with the varying scale and need of the corporates it serves.

3-month equity-free accelerator program; lighter touch than YC or Techstars

Fund checks vary, depending on size, round, etc.

Launch - Launch is Jason Calacanis’s brainchild. The platform is a multi-layer founder funneling media machine, built on the back of Jason’s brand and reach. Launch supports founders across three segments of ‘early stage’ via its Founder University, LAUNCH Accelerator, and Fund/Syndicates. Founder University is the top of funnel 10-week pre-accelerator helping the earliest founders with the basics (MVP, business model, marketing, pitch), and runs at the highest volume with 3-4 cohorts of 80+ founders per year. Typically, the team then invests in the top 10% of Founder University graduates and/or cycles them into the LAUNCH Accelerator, which is more concentrated on smaller batch companies starting to get real traction. LAUNCH Accelerator whittles it down significantly to 10-14 founders per cohort a couple times a year. Jason and team then follow on in the breakouts via his fund or syndicates. The funnel is broadened at the top by Jason’s massive media presence (All In, This Week in Startups, and Angel) that can also serve as microphone/marketing tool for the Launch portfolio companies as well.

Founders University: $25K for 2.5% or $125K for 7% ($1M or $1.8M post, respectively)

Tuition is $500 for founders, reimbursable if you attend all programming

LAUNCH Accelerator: $125K for 7% ($1.8M post)

Fund/Syndicate Checks: variable

Note: take all these check amounts, cohort cadences, and class sizes with a grain of salt, as all of these various programs are constantly evolving their models.

Regardless of model, starting an accelerator is a herculean lift. You can see from the examples above how many are financed through accompanying businesses, whether that be media, events, corporate partnerships, or some mix. It’s a very heavy flywheel to start. You need your programming to have a distinctive brand, your ecosystem to offer unique advantages, and your model to survive long enough for these bets to pay off. To run more intensive services requires a variety of resources, none of which are cheap, particularly if you’re going to have a physical presence. The management fees on a pre-seed fund alone likely don’t cover the requisite burn either. So, you basically have a deeper J-curve than traditional VC funds sitting on top of an inferior cost structure. This is compounded when you consider that most accelerators are engaging startups at the earliest of stages, thus have the longest time to liquidity even if their investments do well.

You also need a unique wedge to overcome the adverse selection of being a nascent venture platform. Multiple factors cause this inertia. Any founder worth their salt, especially with previous successes, is going to gravitate toward established brands with track records of excellence. Consequently, your talent pool could potentially be comprised of less experienced founders or less compelling ideas. You’re also likely to overindex on first time founders, as they are less likely to have the pitch polish and investor network to win funding on their own vs. repeat founders that have previous touchpoints with investors as well as other builders (even if their first rodeo wasn’t a slam dunk success). This adverse selection alone could be reason enough for broadening your portfolio bets, in hopes of catching outliers in an inferior pool of options.

As with everything in venture, there’s also a massive power law at play. The YC’s of the world have created enough density to form a supermassive black hole for talent. A select few players have the kind of mindshare that becomes a self fulfilling prophecy- talent attracts talent creates winners attracts talent… Thus, new accelerators often draft off the success of a bigger brand (ex: a16z Speedrun) or counterposition through a very specific wedge. A prime example of this would be something like Harpoon’s Black Flag program, which I wrote about last week. Harpoon has established itself as one of the premier defensetech investors, and has leveraged this moat to launch a national security-centric accelerator program called Black Flag. They’ve also augmented the program’s gravitas by partnering with other heavy hitters in the space like Shield Capital and In-Q-Tel (the intelligence community’s VC arm). In all cases, it still requires selling the best builders on why you’re the partner of choice, and why they should pick you over other S-tier funds.

Hence, aura farming. You’re selling the dream that “Uber once passed through these hollowed halls! And you could too!” to fuel the self-fulfilling prophecy you need to perpetuate. Like the startups they hope to back, new accelerators must build the magnetism of a messianic cult. Whether that brand’s whacky, exclusive, aloof, patriotic, or ‘mad scientist’, working with founders is a human business and you’re cultivating a tribe around your banner. Broader reach and a more polarizing presence expands the pool of possible founders for matriculation while concurrently filtering for the builder archetypes you want to back.

That’s an element of why so many of these platforms have media-savvy partners at their head. Adam Draper, Joshua Baer, Jason Calacanis, Garry Tan all have commanding media footprints. Garry Tan has been particularly adept in this regard, scaling the YC media machine while simultaneously leading from the front with his own massive Youtube channel and Twitter following. The idea of VC as media is not new. We’ve seen this strategy proliferate as the industry got more competitive, and players relied more heavily on brand to differentiate. There have been acquihires like Turpentine (a16z), DIY’s like Pirate Wires (Founders Fund), and any number of other independent players like Sourcery, TBPN, and Not Boring that have leveraged mindshare into investment access.

But, with all this smoke and mirrors, founders should be mindful of the statistics at play when considering the value of accelerators, whose capital often isn’t cheap. Fellow founder referrals are gold in this business, and that can help to see past the patina online. “Sure, you have two unicorns in the last decade. Out of how many startups backed? A billion? Sick, your success rate is actually worse than random chance. Oh, and you gave my buddy a check and were nothing but extractive thereafter? No thanks.”

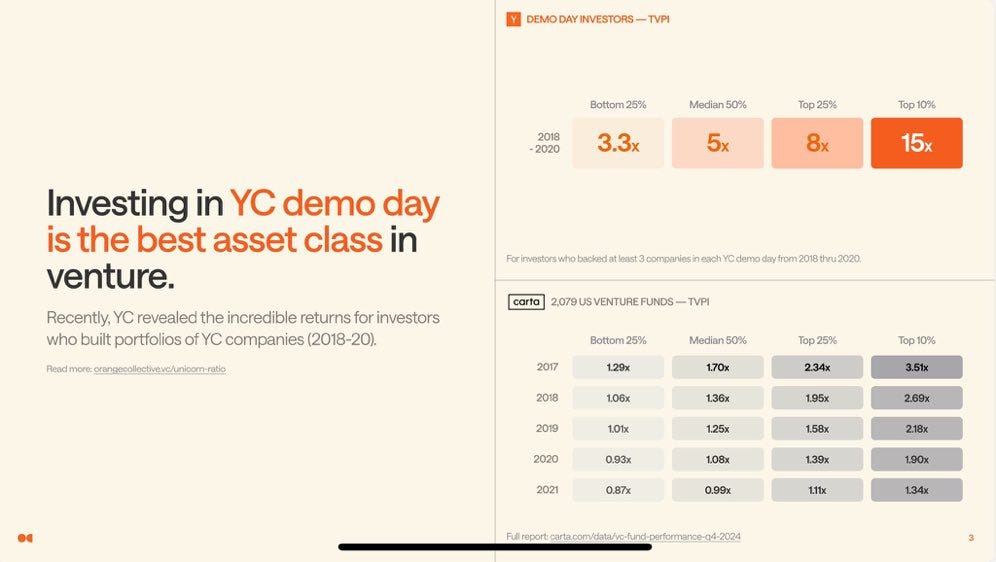

This is one reason I have so much respect for Garry Tan sharing YC’s hit rate:

But even this billboard includes a bit of subtle misdirection – conveniently picked 2018-2020 cohorts (a period which would have been primarily software startups massively marked up through COVID + ZIRP thereafter) vs. the total life of YC funds (2005). It also represents TVPI, which isn’t necessarily realized gains. This exemplifies yet another one of the funny dynamics of VC land: no one is incentivized to show their scorecard.

Again- spray, pray, and yap away.

It’s even funnier when you begin to learn how many VC’s sing the praises of deals where they got absolutely hosed. Restructuring, pref stack, dilution, or any number of other factors could mean that an early Reddit investment was actually a total wash, yet investors have every incentive to absolutely celebrate the founder in public and champion that position as their genius investing acumen.

Of course, economic reality catches up sooner or later – DPI, DPI, DPI. But that’s typically shouldered by the begrudging LPs on the back end, unseen by the founders dropping into the top of funnel. You can run a shit accelerator for a decade before anyone gets wise to the realities of the situation. And if you’ve got a cash flowing side business to boot, you can literally run an accelerator long enough to all but ensure that you eventually have a winner. The law of large numbers would suggest that, unless you’re utterly incompetent and your dealflow is trash, you should be able to get into at least a couple unicorns if you’re ripping hundreds of angel checks a year on a long enough time horizon.

Conclusion:

I got a bit cynical here. I really should clarify.

I don’t mean to say that the praying and spraying is all bad, although it can carry that connotation. Realistically, you kind of have to play a very large numbers game if you’re investing at the earliest stages. Data is limited, markets are unclear, and mettle is unproven. The accelerators that are run very well are a legitimate boon to the innovation ecosystem. They empower early founders with resources and expertise they may otherwise lack, and help to professionalize many, many ‘two guys and a laptop’ pipedreams into formidable businesses.

But founders should be thoughtful about just how much is marketing in all these lofty promises. DYOR, NFA, find referrals.

For the other side of the coin, young investors should also remember to be discerning as they see those “XYZ-backed” slides in decks they review. These accelerators work at such volume that their stamp of approval can’t be taken as an outsized mark of confidence, particularly when they’re playing a game across hundreds of companies versus the dozen or so picks you might make in your more concentrated fund.

All to say, accelerators, incubators, and especially ✨ecosystem builders✨ are a very funny business. No one’s incentivized to share their scorecard, the human mind is very bad at grappling with power laws, and even the best will produce 80% duds. Caveat emptor.

- 🍋