Some Scallywags You Might Love

Business Models and Bangers in the Black Flag 100

Welcome to Words with Wynn! If this is your first time reading my content, and you’d like more of my weekly musings, subsribe below:

I recently came across Mike Annunziata’s piece, Five Business Models We Love, and its reference to Morgan Housel’s Betting on Things That Never Change.

Rereading the latter was a good refresh for my investor psyche, and exploring the former a good lens for my own startup scouting. Perusing Mike’s piece was stimulating, but learning requires action So, I thought I’d apply his framework to the Black Flag 100 to see who emerged.

The Blag Flag 100

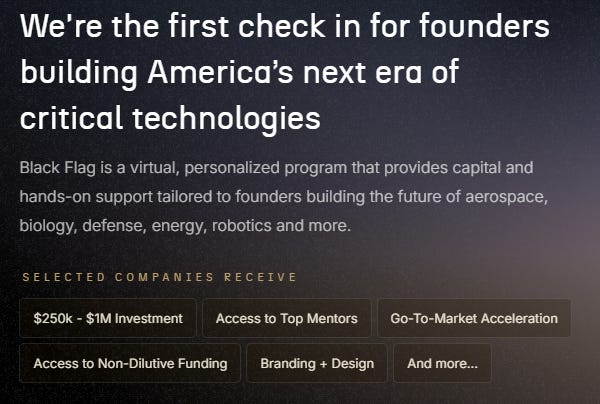

Black Flag is a program spun out of Harpoon Ventures, and is building one of the best deep tech ecosystems around. It’s run by Harpoon in collaboration with Shield Capital and In-Q-Tel (the U.S. intelligence community’s strategic venture arm), and aggregates a wealth of resources for founders building in national security including non-dilutive funding support, a deep bench of mentors, and direct connections with leaders across the government.

A side note I’ve been thinking about –

It’s interesting that they also emphasize branding + design as an element of their support:

It may sound soft for the hard tech space, but I’ve really doubled my conviction in the importance of branding (and by extension, distribution) for deep tech startups. Many are run by gigabrain engineering types building incredible things, but ignoring the battle for attention puts them at a distinct disadvantage. A sexy brand, and a well-distilled mission helps to attract customers, talent, and investment (see: Rainmaker as a marketing master class).

I believe that this is why we’ve seen the explosive trend of hyped launch videos coming out of the likes of YC, probably emerging on the back of Anduril’s badass product videos last year. And more specifically, I believe that branding and/or marketing reach is one of the unique ways that an external partner can really add value for founders. Why else do you think every VC has a podcast?

A great example of this, and a firm whom I respect for it, would be Space Cadet Ventures– all of their work is sleek, their decks incredible, and their LP drops differentiated.

The Black Flag 100 itself is an aggregation of startups nominated by 300+ late stage deep tech founders. Their total universe was 500+ companies, curated down to the top picks by the Black Flag team. A couple stat sheets on sector and stage:

So, they’ve got the bona fides for some interesting deep tech picks, and I thought the Black Flag 100 would be a ripe ground for filtering startups through Mike’s framework to see what caught my eye.

Five Business Models We (might) Love

1. Recurring Revenue Infrastructure

These are companies that build real-world systems and monetize them with usage-based or subscription pricing. The business grows as the network grows, and the revenue is predictable.

Aetherflux is insanity. Founded by Baiju Bhatt (co-founder of Robinhood), the team is launching an array of satellites into Low Earth Orbit (LEO) in order to gather uninhibited solar power and beam it back to earth. What?

The idea is crazy. Crazy enough that it just might work. And the repercussions of such a system would be profound. Given the massive costs of terrestrial power generation, and the significant losses in power transportation, this scifi idea could upend power availability with a multitude of knock-on effects– everything from supply chains for the military to urban planning and nationstate infrastructure.

There’s precedent for this kind of technology with Caltech’s 2023 breakthrough successfully beaming 200 milliwatts down from space and DARPA’s recent 800 watt wireless power delivery over five miles. Granted, these were miniscule power levels: the DARPA example transported about enough energy to pop a bowl of popcorn. Both are very early, and clearly the Aetherflux team will have to harness significantly more power over vastly farther distances, but these examples serve as proof points that the idea can be done.

I view this project as one of those unique startups building at the intersection of multiple declining cost curves while capitalizing on the second-order effects unlocked by recent technological breakthroughs: collapsing launch costs, advancements in sensors/transmitters, on-board compute, solar panel efficiency, emerging space economy supply chains, etc.

Hence, it’s a long and ambitious bet, not unlike the SpaceX and Vardas of the world, but the spoils of success would be massive.

This fits well within Mike’s framework, with a growing network value accruing as the underlying infrastructure develops, which will presumably be highly sticky given the insane capital cost of entry in combination with the technological moat you will establish should you be able to make the technology viable.

2. Full Stack Vendors in High Trust Markets

In regulated or risk-sensitive environments, customers prefer one responsible counterparty. If you can deliver a complete solution—hardware, software, service—you build trust and stickiness.

Nuclear

I don’t want to beat a dead horse on nuclear, but I think the entire category pretty well fits this idea. Multiple startups in the emerging nuclear renaissance were included in the Black Flag 100, including hometown (Austin) heroes Aalo Atomics and Hexium:

It’s a developing race to market for SMRs with the Department of Energy recently announcing their selection of 11 reactor companies to help expedite the testing of advanced designs. But more than that, we’ve seen a resurgence across the entire value chain from startups like Founders Fund backed General Matter (enrichment) or Standard Nuclear (fuel production) through to ‘AI for Nuclear’ software like Atomic Canyon. TBD precisely where value accrues here, but it does seem like there’s significantly more competition at the SMR/reactor link of the chain vs. even more regulated components like enrichment where the government and commercial players will likely source from only one or two vendors. That said, the mind-boggling power demand of the AI arms race could represent a multi-winner market on the SMR side.

Maybe alittle on the nose for Full Stack Vendors in High Trust Markets, but Andromeda is racing ahead with an autonomous surgical assistant, starting with endourology. They’ve built a tablet-operated platform to help urologists perform Holmium Laser Enucleation of the Prostate (HoLEP) – a gold standard but technically demanding procedure for enlarged prostates.

The integration of robotics and automation into the operating room continues to be slowgoing, despite many of the biggest players in the world attacking the opportunity. Intuitive Surgical has been working on its Da Vinci platform for over two decades, initially operating as a laparoscopic surgical assistant and now layering in incremental automation.

Andromeda is intriguing in that it’s already semi-autonomous, with the surgeon today initiating and supervising the procedure. Where systems like the Da Vinci rely on joystick-based mirroring of the surgeon’s fine motor movements, the Andromeda system is more akin to auto-pilot that commercial airline pilots utilize today– manual for a few touches, but largely self-directed with supervision. The startup has been accruing validation for its technology, performing over a dozen clinical procedures in Chile and New Zealand.

The first mover advantage within robotic medicine could provide a significant moat, as well as a well-fortified beachhead for product expansion. Once trust has been built at the hospital buyer level, it is likely that adding additional use cases to your existing system and selling those through will be easier than a de novo device or player attempting to break in.

3. Tools That Become Platforms

Start with a narrowly useful product. Over time, expand into adjacent workflows, integrations, or systems of record. These businesses often start as tools and evolve into infrastructure.

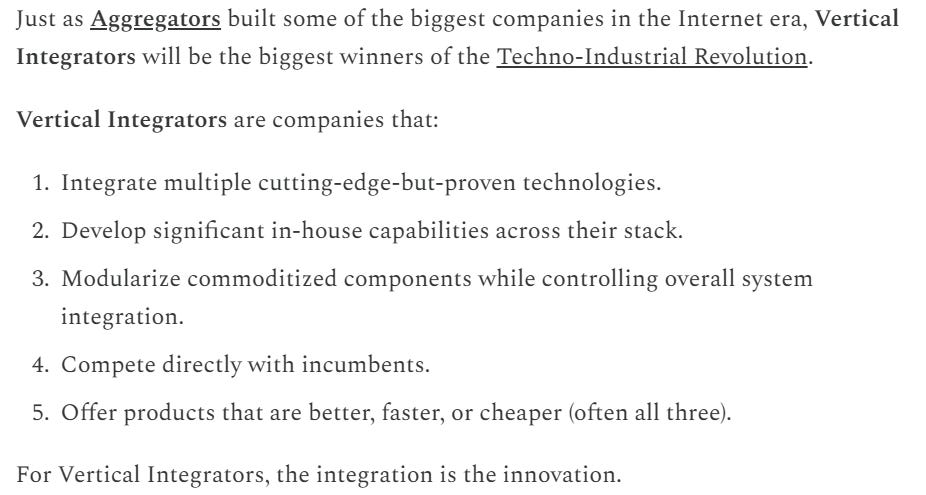

The ‘Tools Become the Platform’ lens pairs nicely with another one of my favorite deep tech frameworks: Packy McCormick’s Vertical Integrators thesis.

Packy’s two-part treatise is summarized above, and I think it is a useful mental model for these kinds of hardware heavy industrial disruptors vs. vertical/horizontal software type products that require a different approach for consolidating their value chain.

Durin could be a Gundo Bro poster child.

The startup is helmed by the fearless Teddy Feldmann, with grand ambitions of building a next generation integrated mining titan to secure American minerals. The stakes are huge, the tech is dirty, and the market is massive.

Ambitious from inception, Durin calls its shot in both name and vision. The startup’s name pays homage to the altar of Thiel, pulling directly from the Lord of the Rings universe to invoke mythical lore and Silicon Valley progeny. Tolkien’s Durin was the greatest of the dwarven kings, and referencing Middle-earth mythos is a beloved tradition of American Dynamist darlings:

Palantir (data analytics) - named for the seeing-stones that allowed distant communication and surveillance across Middle-earth

Anduril (defense tech) - Aragorn’s reforged sword, the Flame of the West

Erebor (crypto bank) - the Dwarves’ ancient stronghold and treasure hoard

The company itself is starting with a specific tool in a specific link of the mining value chain as their first product to gain a foothold in the market.

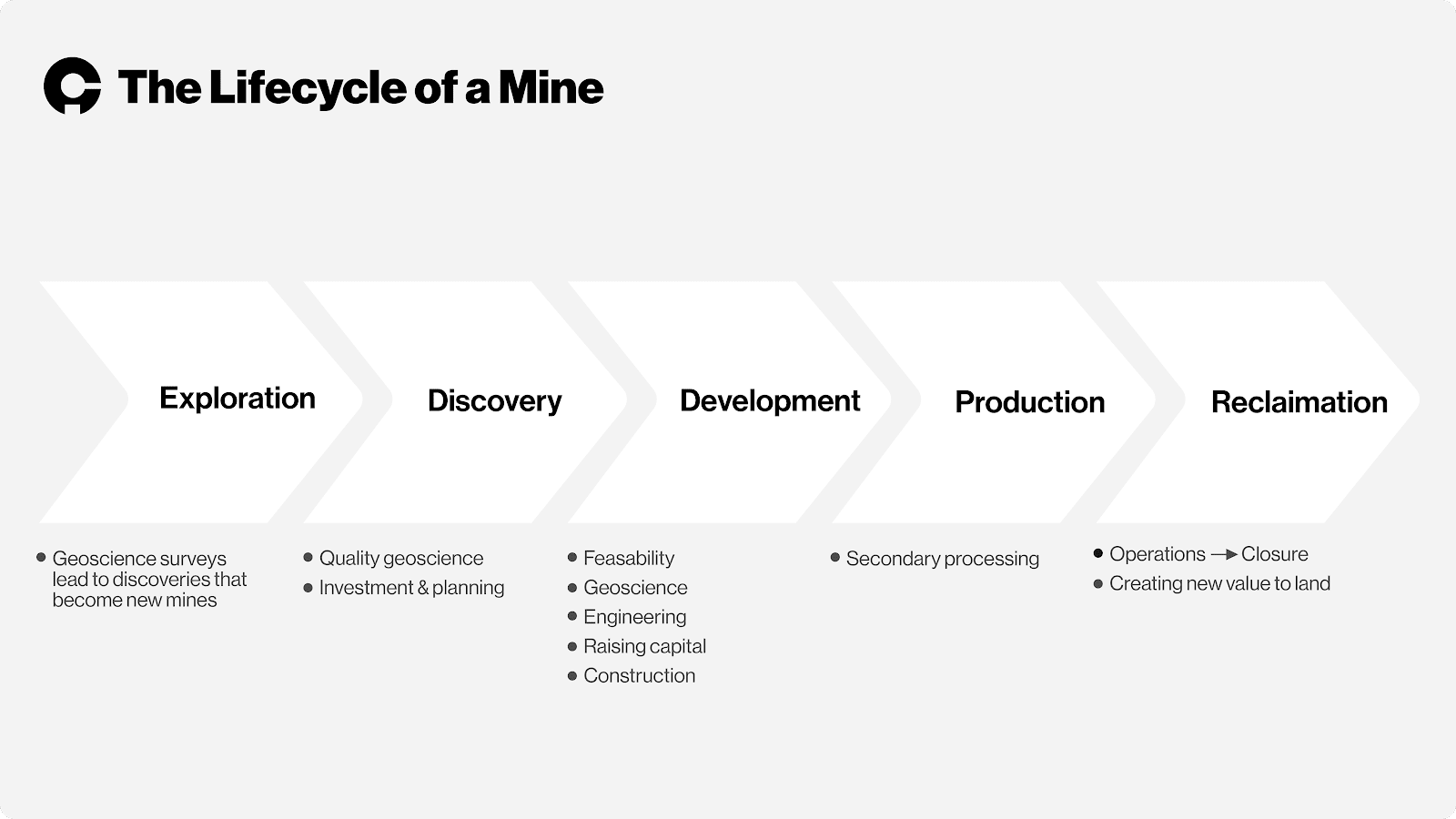

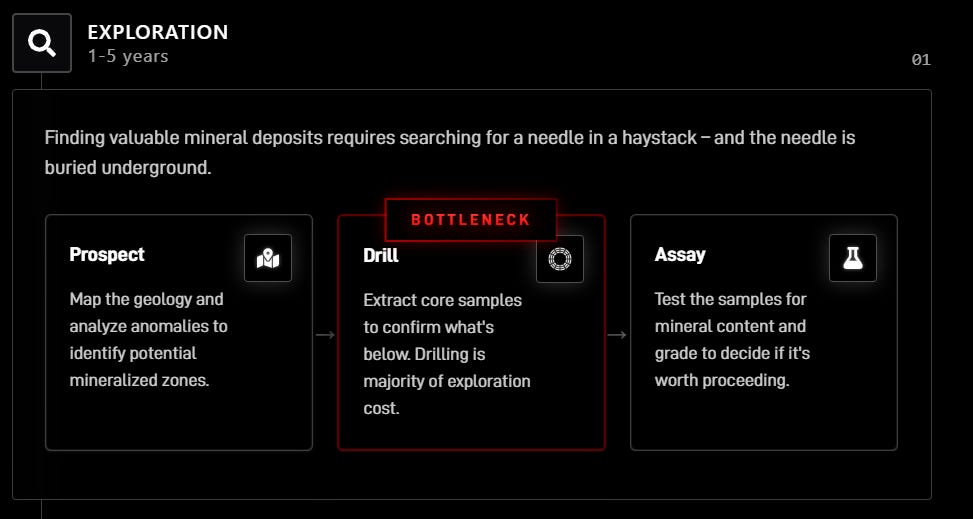

For context, developing a new mine is an extremely long and complex process, with a number of players shouldering different levels of risk all across the lifecycle:

Typically, a mine starts with land acquisition and prospecting rights (usually by ‘wildcatters’), followed by geological surveys and surface sampling. Once there’s enough data to form a hunch about a particular parcel of land, then comes core drilling where the wildcatter will hire a third party contractor to drill and pull dozens of deep samples to validate the underlying minerals. These samples are then fed back to geologists, labs, and auditors to thoroughly assess the value and begin making the case for developing the underlying. Given the incredible investment required to develop a full-blown mine, you can imagine the importance and thoroughness of this validation step (many cores to be drilled). Once a compelling case can be made for development, the wildcatter or junior miner typically sells the land to or partners with major mining players with the scale, balance sheet, and expertise to build the mine itself.

Exploration and core drilling are the steps that Durin hopes to improve, finding and validating more mineral deposits faster to accelerate the development of domestic and allied rare earth mining operations. The team is integrating a number of off the shelf parts to build semi-autonomous core sampling rigs in order to perform this piece of the value chain cheaper and faster.

Strategically, it makes sense that a startup would attack this link. It represents more consistent work with less risk and lower capital requirements. But even within core drilling, Durin’s hoping to build an edge and operate with improved margins by developing their own rig and sensor suite as opposed to existing players that are more service contractors (buying/leasing rigs from OEMs and providing the labor to operate them). By their estimate, core drilling is a highly manual endeavor and can be as much as 80% of the costs of an exploration project. Teddy & Co. believe they can provide this service in a more streamlined offering by manufacturing a semi-autonomous drill in-house and operating it more efficiently.

From there, Durin can evolve from tooling to platform, layering assays, geophysics, and analytics into a vertically integrated exploration engine.

4. Data-Exhaust Flywheels

Some companies generate valuable data as a natural byproduct of their core operations. That data can be used to build intelligence layers, drive new products, or create entirely new revenue lines.

Orchard Robotics is building an agricultural data machine. If data is oil in the age of AI, then this team is prospecting the Permian. Where many startups have stumbled building expensive robotic labor solutions for the agricultural sector, Orchard has taken a different tact.

Charles Wu and team have developed a mountable camera system with the ability to capture over 100 images per second, recording data about every fruit on every tree within a grower’s orchard. For scope, orchards can have millions of trees growing hundreds of millions of fruit across thousands of acres. It’s an incredibly complex data question to provide tree-by-tree analytics in an economical way (farmers historically leaned on statistical sampling to make harvest-level decisions), especially given the terabytes of data required in generating reams of images for every tree. Couple this with the challenge of developing farm-sturdy hardware that can operate rain or shine, and you’ve got a particularly thorny problem.

The fidelity of this data is key in driving effective decision-making processes for farmers, and can be gathered in a non-intrusive way by simply strapping Orchard’s camera to existing equipment like tractors and carts.

Orchard then offers its FruitScope OS as a comprehensive farm management software, leveraging the data provided by its camera stack. This razor+razorblade business model, placing low margin hardware coupled with a high margin software stack, is interesting because it provides Orchard with a unique strategic position. As opposed to other startups that must scramble to gather data for their capital-intensive robots, Orchard has the unique vantage of picking from commoditized hardware players in the future and operating as a higher margin intelligence or data layer for its partners.

This appears to be where the company is potentially going with its forthcoming Canary product, which it is marketing as an AI powered decision-making tool to improve the entire growing lifecycle - pruning, spraying, irrigating, hiring, harvesting, marketing and selling, distribution, etc.

5. Real Asset Arbitrage

These businesses find overlooked physical systems—cooling, sensing, RF, etc.—and apply modern technology to reprice risk, lower cost, or create new economic leverage. They often don’t look exciting from the outside, but they work.

Parallel Systems is a bit closer to home. This one isn’t actually in the Black Flag 100, but fit too well to pass up. I live about 50 feet from the train tracks that run through downtown Austin, and the daily screeching steel of American Industrial Might led me down the wormhole of “Why isn’t there a SpaceX for rail?”

Founded by three early SpaceX engineers, Parallel systems is developing autonomous, battery-electric freight vehicles.

What interests me about Parallel Systems is not that they will disrupt traditional rail (they might do that), but that they found an orthogonal way to attack the industry that aligns their business model with the existing oligopoly of players.

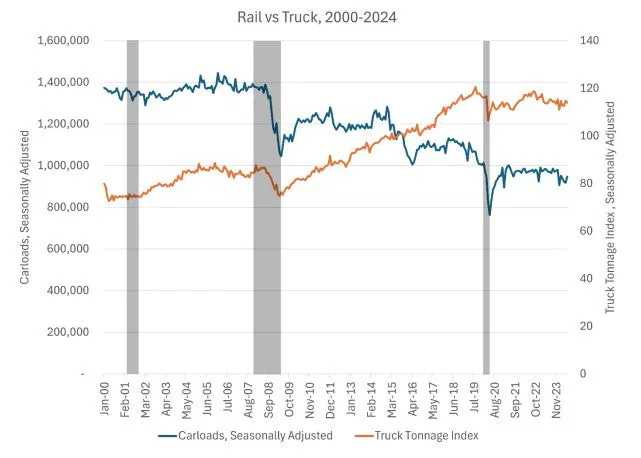

Rail has been getting crushed by freight for the last decade for its lack of flexibility and service deliveries:

Parallel’s wedge into the market is enabling uneconomic (low density) lines to become viable, thus expanding the market for railroads and helping them to take share back from freight. And when you consider the difference in market sizes, trucking is 10x rail by revenue, even a fractional shift in share could be a massive outcome for Parallel.

Then they become infrastructure. Parallel is a heavy industry play that helps their customers win. It’s a B2B2B value chain whereby they support the Tier 1 railroads, allowing them to improve their service and expand their offerings to shippers. Shippers are happier with the consistency and additional optionality, and thus steer some of their choices from freight to rail. Once integrated, Parallel’s systems become an irreplaceable component of the rail service offering, and the regulatory challenges they’ve scaled are digging an increasingly deep moat in their wake.

The company also has an interesting second order effect of reducing carbon emissions and abating overall congestion. They’re utilizing an electric drivetrain for their system, which saves of course on pollution at the margin, but where I find their model compelling (from an externalities perspective) is that success for Parallel potentially reduces trucks on the road and city-wide congestion around major ports and rail hubs.

Bonus: Airship Industries

A Black Flag 100 that does fulfill a similar idea to Parallel is Airship Industries. Backed by Packy and pointed to as an example of the Vertical Integrators that he loves, you can learn more here to decide whether or not founder Jim Coutre is full of hot air.

Conclusion

Perusing the pirates of the Black Flag 100 fires me up for the future:

It’s a treasure map of builders and businesses trying to upend industries. Mike’s framework is an excellent tool to sharpen one’s thinking about which of these players may emerge victorious. Of course, compelling business models alone do not unicorns make (it’s the blood, sweat, tears, and grit of the founders pushing them forward), but studying how they interact and where they sit can help inform your understanding of why some innovations win.

The privilege of being a venture capitalist is meeting the ambitious minds ideating these technologies and watching them reinvent the business models they enable. It was a pleasant surprise to see a few of our founders grace the Black Flag 100, and even more exciting to note the new ones I’d like to meet.

Finally, if you’re a pirate that may have missed the list. Even better. Drop me a line.

- 🍋