Will Vibe Coding Eat Design?

A Modern Scorpion and the Toad

Welcome to Words with Wynn! If this is your first time perusing my content and you’d like more of my weekly musings, subscribe below:

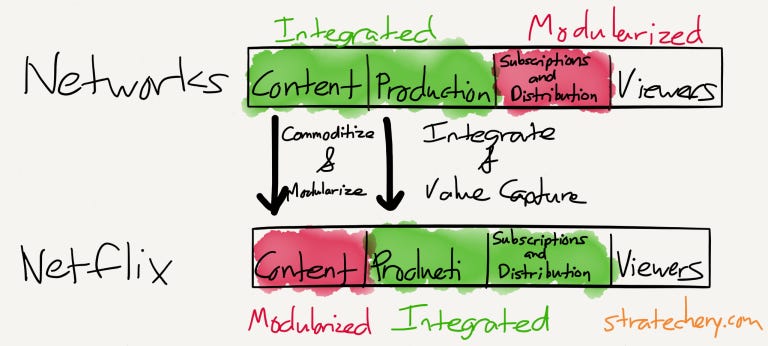

In the early days of streaming, there was once a strategic conundrum of great debate: could Netflix become cable before cable became Netflix?

Netflix was a disruptive aggregator that thrived by modularizing content while integrating production, subscriptions, and distribution:

The startup had built a platform that aggregated content from all the producers/studios, and owned the infinite distribution that the internet had enabled. This allowed Netflix to scale rapidly, reaping the decreasing CAC that comes with being an aggregator.

As the streaming giant grew, an inevitable tension began to emerge: this type of market consolidation inevitably squeezes suppliers (the studios/networks) as the aggregator A) gains buying power B) increasingly commoditizes them. Netflix was destined to bite the hand that fed; a relationship which was once complimentary for the content suppliers, gaining distribution, would eventually compress their margins. The tension between these two increased exponentially with Netflix’s share of the market.

Thus, the race was on. Could Netflix commoditize its suppliers before they worked out an alternative strategy for distribution or differentiation?

Eventually, everyone and their dog became a streaming service.. But not before Netflix was able to flex its balance sheet and backward integrate, producing its own prestige content. For a rough timeline, Netflix began streaming in 2007 and Hulu launched in 2008, but was largely ad-supported vs. subscriptions. Although there were other attempts (Amazon, etc.) along the way, the streaming wars themselves really didn’t ignite until the late teens with the launches of Disney+, Apple TV, Peacock, and HBO Max. By then, it was far too late. Netflix had been producing its own originals since ~2013, with major successes like House of Cards and Orange is the New Black before mega hits like 2015’s Narcos and Stranger Things. The platform’s leverage was established and, although the content landscape has fragmented in recent years, it still remains in pull position today.

I think we’re destined to see a similar dynamic play out today between design software and vibe coding platforms. From my personal use, I’ve been wondering if Replit eats Figma before Figma can eat Replit.

Right now, these platforms are more-or-less frenemies. Vibe coding empowers designers, so Figma is happy to integrate with whomever would like to plug in. Conversely, players like Replit are happy to tap Figma’s massive user-base of tech savvy customers to leverage distribution. Symbiotic.

But eventually, this feels like a modern scorpion and the toad situation:

Today, Figma is the bigger fish swimming in a different pond. Their target audience historically has been designers and teams building digital experiences. They’re approaching $1B ARR (still growing 46% YoY, mind you) across 13 million monthly active users. This is compared to the leading vibe coders like Replit and Lovable, who are both doing around $100M ARR on significantly smaller user bases of software developers and the ‘coding curious’. Replit claims 500K ‘professional users’ and Lovable claims 180K paying subscribers/2.3 MAU.

The scales and targets are different for now, but I believe their end goals are destined to collide. Both vibe coders and design platforms are ultimately tools for democratizing software creation. They’re similar accelerants for the arc of accessibility, an idea I previously explored. Although Figma’s bread and butter is professional designers working cross-functionally to bring ideas to life, they specifically note in their S-1 that about ⅔ of their users are non-designers. I imagine that Replit’s user split is probably in the same ballpark, with offerings for professional-grade devs but a stated goal for anyone to create software.

Just look at the company visions:

Some of it is corporate slop, but there’s a clear focal point of their mutual aims: be the go-to platform for creativity expressed through software.

Which begs the question: who will eat whom?

The ouraboros has already started to feast:

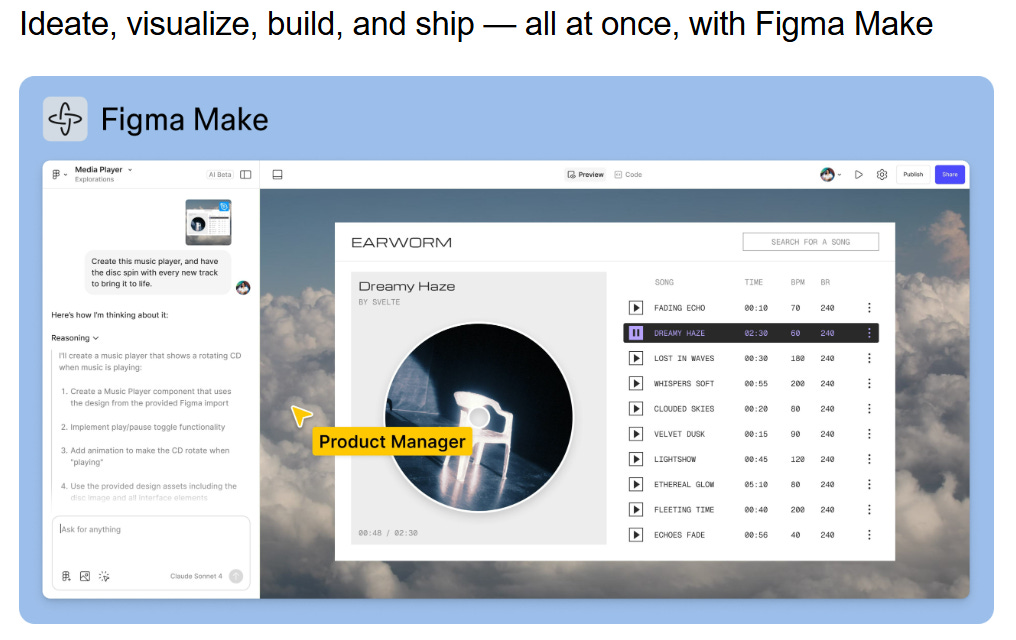

Replit has robust integrations to simply flip your wireframes from Figma into Replit’s platform, then build out the functionality via its Agents. But they’ve also bolstered the native UX functionality with design-phase planning in new projects and tools like Visual Editor, which allows you to make edits directly to the UI with real-time code updates. Conversely, Figma has always supercharged the speed to ship software with resources like Figma Dev Mode, but now they’re expanding their purview with native prototyping via Figma Make:

This convergence creates a very interesting strategic dynamic. If you’re Figma, you kind of want to do the Netflix thing. Continue aggregating a very specific and very valuable audience while commoditizing your compliments. As long as you own the distribution, you’re in a prime position to be the middle layer of creation for your users while simultaneously leveraging increasingly interchangeable AI models for the actual development. In and of itself, Replit does not build the underlying LLMs in-house, which implies that there may be an opportunity to eventually disintermediate the software creation player. If you’re Figma, you want to continue expanding your actual software development offering, leveraging whichever model as the back-end of your infra. This allows you to provide an improved user experience while capitalizing on market competition to provide the intelligence (ideally, helping to maintain your margins). If Figma Make gets sophisticated enough with its prototyping, when would I ever leave to Replit?

So, where’s that leave Replit? If you’re in their shoes, do you really want to go to war on the aesthetic front for that user-base, or is the TAM big enough simply drawing in normies like me? Hard to tell as paths converge. My journey to Figma came via my janky prototyping in Replit and a desire for more tasteful UI. But then-again, in a world where software becomes content maybe there are more attractive vectors for differentiation.

The same way that models themselves potentially get commoditized, I think that vibe coding likely does as well. Not that a huge player won’t come out of that space, but that competition will be fierce and margins likely compress. There’s already a crowded field of players coming for this crown. The Replits and Lovables of the world are trying to onboard the next generation of software developers while a score of other vibe coding platforms are going after prosumer and enterprise. All the while, the LLM developers themselves are offering ever more agentic features natively.

This is why the end platforms will be defined by more than simply code. My ChatGPT interface can rip code with the best of them today, but it lacks the context, integrations, and capabilities to deploy full stack creations. Sure, perhaps its independent agents will be able to take those steps for me eventually, but having an integrated solution on a single platform will have significantly less friction.

The lift for design platforms to integrate better models into their stack is likely lower than the technical know-how it will take to deploy full user-grade applications in a one-stop shop. Plus, providing the infrastructural back-end to enable your creators to flex up and down with your platform as they scale will be important. Replit wants to become as Shopify-like as possible, allowing builders to go from idea to deployment to 100,000 customers with their tools, all while living within Replit’s ecosystem. As we’ve seen elsewhere with the likes of Roblox, providing the tools and infrastructure for user creativity and monetization is a highly lucrative position to occupy. Perhaps the market bifurcates into code creation layers for rapid prototyping through the likes of Figma, while the Replits of the world are forced to move more vertically in order to offer a differentiated solution for their users.

That’s the current landscape.

Figma Make is a fun prototyping tool, but lacks the depth to really ‘ship to prod’. Could they build these capabilities in-house? Maybe. But it would be slow and they probably lack the real expertise to stand up the needed infrastructure. A more interesting question is whether or not they should simply buy their way into vertical integration..

Figma IPO’d about a month ago, adding ~$412M in cash to their now $1.2B warchest. They’re doing over $1B ARR at this point at 90% margins, growing almost 50% YoY. On top of that, they have about zero debt on the balance sheet. Against their $28B market cap, a material acquisition of an agentic coding platform is well within reach.

There’s precedent for such a move:

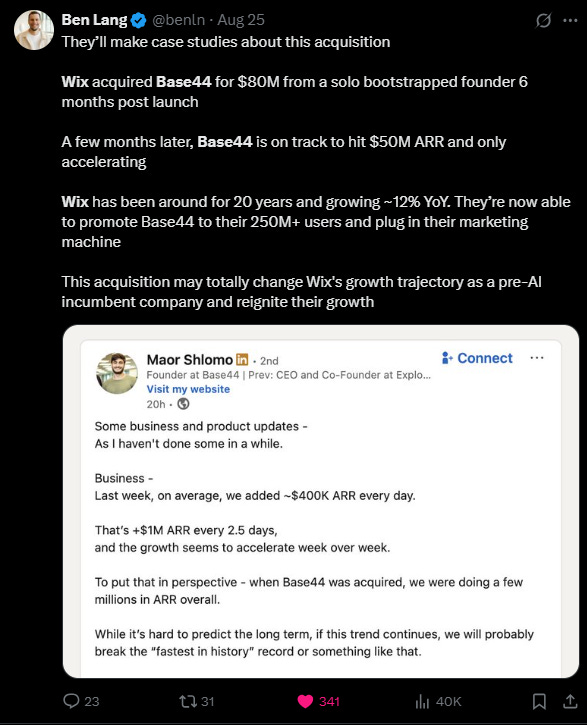

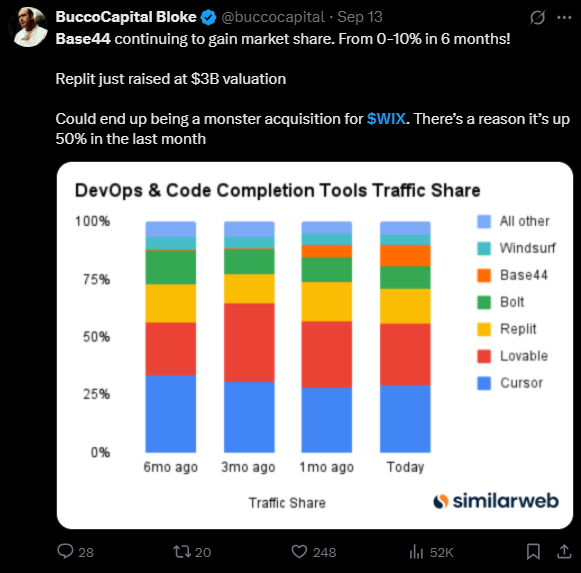

Figma would be quite a bit later to the game vs. someone like Wix who was able to scoop up Base44 for $80M (amazing buy so far), but nonetheless the acquisition route would get them up the learning curve far more rapidly. All the while, Figma’s seeing its core business attacked by such upstarts as AI-native website builder Framer ($2B val/500K MAU):

Ultimately, we are living through a stunning period of tech disruption. Figma’s future, like every incumbent on the block, will be defined by its ability to adapt to an agentic paradigm. The cost to ship is collapsing, and simple prototyping on their platform may not be enough to maintain the company’s moat around software creation.

Admittedly, it’s far too early to suggest that Figma has stumbled with its AI implementations; they’ve been generally well received. But this could be a moment where cracks begin to form. Their core business is under assault from upstart players, and complementary products are gnawing at their sides. With its recent public offering, Figma has the ability to leverage public markets in a way that its competitors cannot. If their scale and IPO have lowered the company’s cost of capital, an acquisition like Replit might just be the opportunity to eat vibe coding before the scorpions come for design.

- 🍋