More Than a Flight of Fancy

Will All Our Packages Be Delivered by Drone?

Welcome to Words with Wynn! If this is your first time perusing my content and you’d like more of my weekly musings, subscribe below:

Not so long ago, it was magical that we could press a button on our phone and have items miraculously appear at our doorstep. We take it for granted now, but the implementation of two-day delivery by Amazon in 2005 (and same-day delivery around 2009) was a logistical feat. Today, consumers are accustomed to max convenience with max speed– Amazon delivers your package the same day, Uber drops your egg rolls in 30 minutes with 99% accuracy. With the blazing speed of modern logistics and the hyper-competitive retail value chain, where else can efficiencies be rendered?

One possible avenue is last-mile logistics. The final mile is the least efficient, most expensive part of almost any consumer delivery. It’s the stretch in which your economies of scale break down while your labor intensity rises. With cusping advancements in autonomy, there are a number of startups attempting to rethink this link in the supply chain.

Drone delivery, what used to seem like a Jetsonian idea, is rapidly becoming a reality. Startups are attacking this challenge from all variety of angles (ground, air, and sea), but my focus lately has been the fleet of founders zeroing in on electrical Vertical Take Off and Landing (eVTOL) drones to solve last-mile delivery in urban environments. Simply put, delivering your DoorDash via autonomous mini-copter.

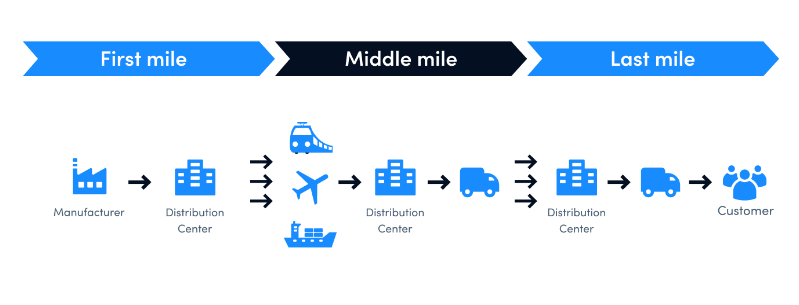

Why Last Mile Is Hard

Last-mile logistics, defined broadly as the final step in getting a product from a distribution hub to a customer’s doorstep, has been the bane of many a startup’s existence. Although technology has enabled numerous advancements in connectivity (ordering from your phone, GPS-location of your goods en-route, etc.), the most challenging component for many of these startups is the translation from bits to atoms. In the late teens, a number of founders leveraged the internet’s organizational powers to create a wide range of delivery marketplaces– Uber Eats, DoorDash, Favor– and tackle the byzantine challenges of delivery itself with companies like Fetch, Parcel, and Shyp. The demand clearly exists and the market opportunity is huge, but any service targeting the last-mile itself is an intensely challenging nut to crack. Why is that?

Last-mile delivery can account for up to 53% of supply chain costs, and for good reason. This is where your economies of scale buckle. Where first-mile and middle-mile can capitalize on single-stop (point to point) fixed routes moving bulk product on the backs of planes, trains, and other large vehicles, your final mile often boils down to irregular pathing with highly manual deliveries. Additionally, your primary distribution centers tend to be located just outside of major city centers along well-maintained highway or rail systems. For your final miles, drivers are navigating congested city streets with more variable driving conditions, compounded by multiple stops along any given route.

So, it’s tough, but attractive. The last-mile delivery market is estimated to be over $175B globally, and over $65B in the U.S. alone. Though, that figure should be caveated when considering drone delivery specifically. Aerial drone delivery is around a billion today, expanding 10x by the end of the decade. Capturing even a fraction of the market would represent a massive opportunity, to say nothing of the possibility of induced demand expanding that pie further.

Why Deliver from the Heavens?

Before considering the ‘who’ of drone delivery, I think it’s important to consider the ‘why’. Initially, my gut reaction to aerial drone delivery was as more of a novelty than a serious, scalable, and potentially disruptive delivery platform. I had so many skepticisms— airspace considerations, liability (drones falling out of the sky?), efficiency (single drone + package vs. streetside Amazon trucks), among others. And, while some of those are still valid, I’ve started to think that the juice might just be worth the squeeze.

Fundamentally, it will always come down to cost:

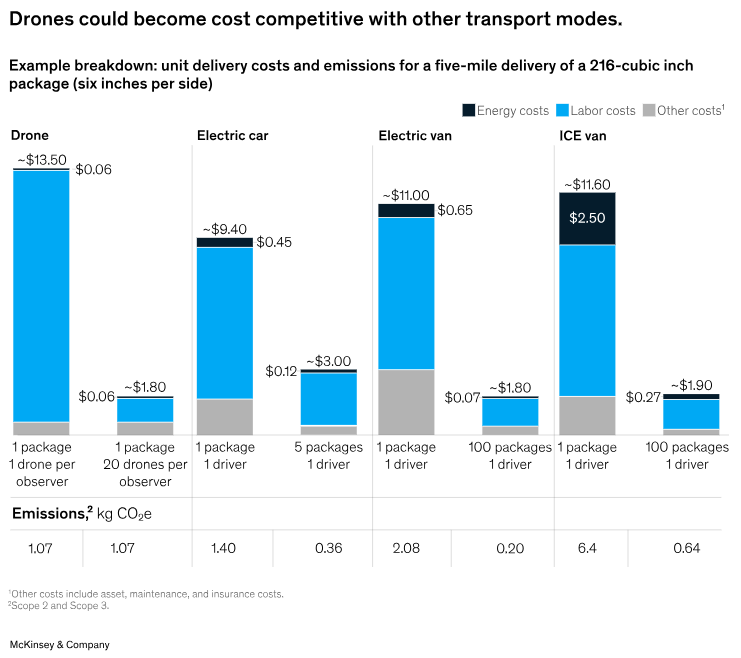

The key is reducing labor costs through scalable drone fleets. Even with the 1:1 drone to package weight limitations, the combined aspects of fleet capabilities and speed of delivery show promising signs of achieving cost parity to legacy delivery channels (cars, vans, etc). And the graphic above simply runs costs today at the legally viable rate of 20 drones per observer, which is the bar that the FAA has allowed for a few startups currently. It’s easy to envision a future where fleets have achieved proven safety standards to scale that number 2-3x, and in fact Wing has been approved for a 50:1 ratio in Melbourne, Australia. Couple this with pathing advantages (‘as the crow flies’ vs. indirect and congested streets) to drive delivery velocity/throughput for the distributor and convenience for the customer, and a more compelling picture begins to emerge.

These cost advantages could all be compounded by network effects as well. If an operator can establish a number of nests across an area, they start to build a network of nodes that can decentralize the delivery chain. This means that, similar to ride sharing, drone operators can shift their swarm resources to the areas with the highest demand. The result could be a more dynamic delivery chain as opposed to hub-and-spoke models which are more rigid.

Time sensitive deliveries are particularly attractive beachheads. On one hand, you have lower ticket, high velocity items like food, where freshness and speed is paramount. Drones can bring both service and sustainability improvements vs. single driver, single package food deliveries that proliferate today (a single drone vs. a thousand pound vehicle ferrying a single burrito..). This market is being attacked by players such as Wing, whom we’ll discuss later, via its pilot with DoorDash. On the other hand, you also have markets with higher ticket, low weight items like blood transportation or temperature controlled pharmaceuticals where speed is paramount, weight is low, ticket price is high, and you can potentially capitalize on fixed routes like pharmaceutical distribution to a hospital. Players like Zipline made their name conquering this beachhead in infrastructurally challenged markets like Rwanda, where the company delivers 75% of Rwanda’s blood supply outside of the country’s capital city.

Drilling down on proximity and weight also helps to envision how broad the urban market can become:

“I mean, if you think about it, 90% of all packages that are delivered into neighborhoods every day weigh eight and half pounds or less. And what’s more interesting- and we’re moving those with 6 to 10 ton trucks- and if you also consider that 90% of those packages sit on a shelf within 5 miles of a customer.. yet that’s not how we’re delivering it.” - Tom Walker, DroneUp (S&D Show)

From my internship in Walmart’s Finance & Strategy Division c. 2017, I distinctly remember leadership discussing the core competency of having a Walmart Store within 10 miles of 90% of the U.S. population, and potentially leveraging these as micro-fulfillment centers. Drones could bring that one step closer to fruition and potentially serve as a key competitive advantage against the Amazons of the world who lack such an extensive physical footprint. If a few parking spaces or an unused rooftop can be transformed into micro drone delivery hubs, that could be a significant driver of adoption and delight for customers:

That being said, this delivery channel isn’t without challenges. By and large, this technology is fairly nascent and has failed to achieve domestic product market fit. Walmart claims that 75% of the DFW population can receive delivery by drone, but the actual utilization is an open question. Frontrunners are certainly growing their deliveries YoY, but the volume is still subscale. A few major challenges include:

Implementation: Logistically integrating into existing businesses for DTC is challenging. Rooftops of Walmarts are potentially interesting, but other markets like food delivery are open questions: Should they come from drone delivery ghost kitchens? Will they be tacked on to the sides of pharmacies? Or is it self-serve lockers?

Zipline’s already way ahead of me with their next-gen platform update - inside, outside, or rooftop (link)

Airspace + noise complaints: The FAA is still refining its framework for regulating these startups, and there have been challenges demonstrating fleet safety in order to scale observer to drone ratios as well as operations Beyond Visual Line of Sight (BVLOS). There are also questions around restricted zones (critical infra, airports, etc.) and noise complaints in residential areas.

Consumer behavior: We are in the early innings of user adoption with obvious concerns around safety and package security.

Competitive alternatives: Autonomous vehicles and ground-based delivery drones have certainly received significant investment, which could bring down costs and render aerial drones less competitive.

Despite these headwinds, there’s still a swarm of players going after this market.

Who’s Building

Zipline - Zipline is one of the clear market leaders, having conducted over a million deliveries across seven countries. The company has amassed a warchest, raising over $800M since inception, and most recently securing a $330M Series F in May 2023 at a $4.2B valuation.

Zipline was originally founded as Romotive, a smartphone-controlled robotics company, by Keller Rinaudo Clifton, Phu Nguyen, and Peter Seid in 2011. The precursor company saw some success, going through Techstars and receiving a $5M Series A from Sequoia, but ultimately pivoted due to constraints around consumer robotics as well as global/societal impact for that original use case:

“The more I thought about it, the harder it was to justify expending my energy on a consumer robotics product that probably wasn’t going to work that well. Robots in the home are a notoriously tough space to crack, and I felt that there were bigger problems I wanted to solve…” - Keller Rinaudo Clifton

This led Rinaudo Cliffton to explore other avenues, eventually piecing together a new founding team to tackle a radically different use case: chronically undersupplied hospitals in rural Africa. In countries like Rwanda, where infrastructure is severely underdeveloped, thousands of preventable deaths occur simply due to a lack of essential supplies– particularly blood. This presented a prime testing ground for aerial drones, coupling the key characteristics above (high ticket, time sensitive, low weight payloads) with a strong willingness to experiment by governments desperate for any solution.

Zipline completed its first delivery in Rwanda in October 2016, and has since scaled its medical supply delivery operations across a number of developing markets including Ghana, Nigeria, and Kenya. The startup has leveraged its first-mover advantage to establish market dominance in places like Rwanda where it delivers an estimated 75% of blood supplied outside the country’s capital city.

Importantly, these markets provided the team with fertile testing grounds to refine its technology stack (navigation, fleet management, package processing, etc.) and establish its hardware supply chain. Zipline has leveraged these learnings to expand into larger, established markets with more competition. While still focusing on middle-mile medical supply delivery, the company also competes in last-mile logistics and has established partnerships with companies like Panera Bread and Walmart in the U.S. Today, Zipline has completed over a million deliveries worldwide.

An aside: it’s totally worth checking out their bad ass delivery system in Rwanda, including an aircraft carrier-like sling shot + grab wire system for launch/landing.

Wing - Wing has a slightly different origin story. The company was started in 2012 as a project within Alphabet’s X (f/k/a Google X). Wing originally explored the delivery of medical supplies similar to Zipline, but made a pivot to broader consumer delivery early on. The startup completed its first deliveries in 2014, and eventually graduated from Google X in 2018 to become an independent subsidiary beneath Alphabet. For the duration of its life, Wing was built by James Burgess and Adam Woodworth, who served as CEO and CTO, respectively. Burgess stepped back in early 2022 for health reasons, with Woodworth remaining at the helm today.

It’s hard to pinpoint precisely how much has gone into Wing, given its subsidiary status. The company sits beneath Alphabet’s ‘Other Bets” line item, which discloses $1.2B in revenue with operating losses of $4.5B, but this bucket also includes projects like Waymo, Verily, and others. That being said, they have offered a few rough figures for commercial traction. In 2023, Wing had completed approximately 350K deliveries (vs. Zipline’s 1M commercial deliveries). This appears to be accelerating significantly though:

“On average this summer, we launched a new drone facility in the DFW area every two weeks. And we’re planning an even faster pace of expansion for the rest of this year and into 2025” - Wing Blog, Oct. 3, 2024

Given the similar timelines from founding through commercialization, it’s interesting to examine why Wing may not have achieved quite the same scale as Zipline yet. Two thoughts— strategy and funding structure. From a strategy perspective, going after consumer deliveries may have drawn more regulatory scrutiny and slowed Wing’s overall time to market vs. Zipline’s high pain point, low regulatory environments like Africa where drone delivery solved a clear and obvious problem. Drone deliveries in countries with challenged infrastructure represent more of a stepwise improvement vs. marginal efficiency gains. Then on the capitalization front, there is little reported for how Google X allocates resources, but one could speculate that being a wholly owned subsidiary shielded the company from market/investor pressures that either A) may have demanded more rapid results or B) provided the virtuous cycle of a deluge of dollars following early traction to accelerate far more rapidly. These are broad speculations on my part.

Another interesting strategic decision is the development of Wing’s OpenSky app. Today, the app helps operators map routes, navigate regulations, and receive approvals for controlled air spaces. But this could potentially be a bet on the proliferation of drones, staking an eventual market position as the base protocol through which myriad independent drone operators will run their machines to coordinate routing. Here’s a great promo video from a drone photographer using OpenSky in his work.

Incumbents - Of course, this space hasn’t gone unnoticed by the incumbents. Amazon, DHL, FedEx and others all continue to explore last-mile drone delivery solutions of their own. Amazon recently scored BVLOS approval for its MK30 drone, and is rolling out drone deliveries in markets around Arizona. Alternatively, Walmart has historically favored partnering with specialized delivery companies, working with Wing, Zipline, and even investing in DroneUp.

Conclusion

It sounds crazy. Crazy enough it just might work. People have been toying with the idea of drone delivery for decades now. Bezos himself (optimistically) predicted in 2013 that drone deliveries could be as close as a couple years out as Amazon began experimenting with the technology.

Today, I think there are a confluence of factors accelerating potential adoption. Moore’s Law has propelled improvements in AI and computing power, boosting drone technology. This has worked in conjunction with the early movers like Zipline beginning to achieve manufacturing scale to march further down the cost curve. But what has really been a black swan accelerant for the drone industry has been the deterioration in global geopolitics (Ukraine, Israel-Palestine, etc.). Ukraine specifically has established itself as a proving ground for the future of warfare, and pushed drone performance and swarm capabilities by leaps and bounds. This is to say nothing of the potential for a near-peer conflict in the South Seas, which of course has also accelerated logistical development within the military innovation community as well.

We’re still a long way from broader adoption, but what once seemed a flight of fancy might be closer than we think.

- 🍋